On December 29, 2022, new federal retirement legislation was signed into law as part of the year-end omnibus legislation. SECURE 2.0 aims to improve retirement outcomes by increasing access to retirement plans, growing and preserving savings, and helping Americans manage competing financial priorities so they can achieve long-term financial security. This expands on retirement policies introduced by the Setting Every Community Up for Retirement Enhancement (SECURE) Act or “SECURE 1.0”, which was enacted into law in late 2019.

SECURE 2.0 is a large piece of legislation with more than 90 provisions. Here is a synopsis of some of the key provisions and their effective dates.

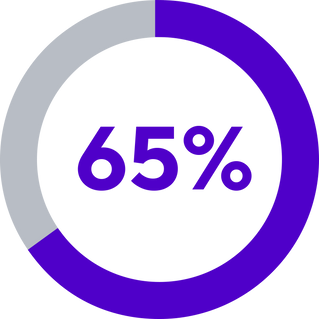

Having income for life is a real concern for many:

Corebridge’s 2022 survey on retirement and longevity found that that 65% of Americans say they fear running out of money more than they fear death.

SECURE 2.0 aims to improve retirement outcomes by increasing access to retirement plans, growing and preserving savings, and helping Americans manage competing financial priorities so they can achieve long-term financial security.

Growing retirement plan contributions

Increase in catch-up contribution limits for ages 60-63.

Currently, plan participants 50+ can contribute an additional $7,500 to their retirement plan. Beginning January 1, 2025, catch-up limits for participants ages 60-63 will increase to the greater of $10,000 or 50% more than the regular limit for 2025.*

Beginning January 1, 2026, catch-up contributions for workers with FICA-eligible compensation higher than $145,000 in 2025, indexed for inflation, must be made into a Roth account.

Matching contributions for student loan payments.

Beginning January 1, 2024, employers can help alleviate the burden of student debt by matching an employee’s qualified student loan debt payment with a corresponding contribution to the employee’s retirement plan account.

Reduce eligibility timeline for part-time employees.

SECURE 1.0 required employers to allow part-time workers who work 500 hours for three years to participate in 401(k) plans. Effective January 1, 2025, this will be reduced to two years and will extend to 403(b) ERISA plans.

Penalty-free access to retirement funds for emergencies could increase savings

![]()

![]()

In the Corebridge survey, 74% of retirement savers say they would increase their retirement plan contributions.

![]()

![]()

73% of those who have access to a retirement plan but have not started saving say they would begin.

Emergency fund needs and the American Worker survey, Corebridge Financial and Greenwald Research, 2022.

Summary

The new law is designed to help plan sponsors take steps to improve their employees’ overall financial well-being and retirement preparedness. It addresses some of the barriers to saving for the future, such as worry about balancing current debt and the potential need to cover unexpected expenses. It also considers longevity and the fact that people could spend multiple decades in retirement.

However, legislation is just part of the equation for helping employees.

We all share an important role in facilitating Americans’ retirement readiness by improving access to and participation in retirement plans, encouraging retirement savings and creating an investment framework that supports accumulation and lifetime income in retirement. Additional steps plan sponsors can take with help from Corebridge Financial include:

Help maximize savings.

Educate employees about the power of compounding and the importance of starting to save as early as possible to help them avoid having to play catch up later in life. But, if they are behind, make sure employees are aware of catch-up options and other planning strategies that are equally important. Corebridge’s financial wellness program, FutureFIT®, helps employees throughout all life stages and personal situations understand where they are in their savings journey and what actions they can take to improve

Educate employees about lifetime income options.

Saving for retirement is only part of the planning process. Generating income from those savings and making it last throughout retirement is the planning step that typically receives less attention. Employees need greater support in figuring out this step and understanding how guaranteed income can be a part of a holistic plan that addresses retirement income shortfalls.

*A participants age for the calendar year is their age as of December 31 – this pertains to all age based catch-up contributions.